Understanding the Notice of Default California Timeline

Notice of Default California Timeline: What Homeowners Need to Know

Receiving a Notice of Default (NOD) in California can be stressful and confusing. Many homeowners immediately fear foreclosure, eviction, or losing everything they have worked for. While a Notice of Default is serious, it does not mean foreclosure has already happened.

Understanding the California Notice of Default timeline is one of the most important steps a homeowner can take. Foreclosure follows a structured legal process, and knowing where you are in that process can help you make informed decisions instead of reacting out of fear.

This guide breaks down the California Notice of Default timeline step by step, explains what happens at each stage, highlights common mistakes, and outlines options that may still be available.

What Is a Notice of Default in California?

A Notice of Default is a public legal document recorded by a lender after a homeowner falls behind on mortgage payments, usually after about 90 days of non-payment.

It is important to understand what a Notice of Default is—and what it is not.

- It does not mean your home has been foreclosed

- It does officially start California’s non-judicial foreclosure process

- It creates a legally defined timeline that lenders must follow

Once recorded, the Notice of Default becomes public record and signals that action is required.

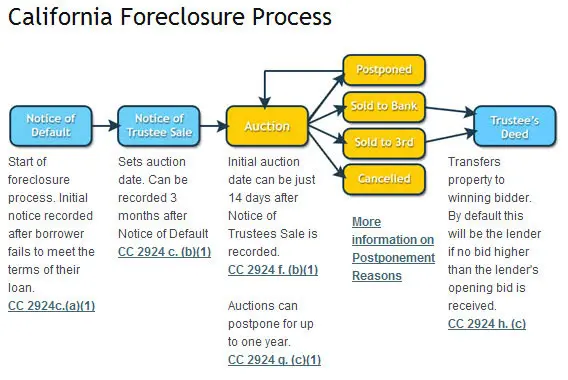

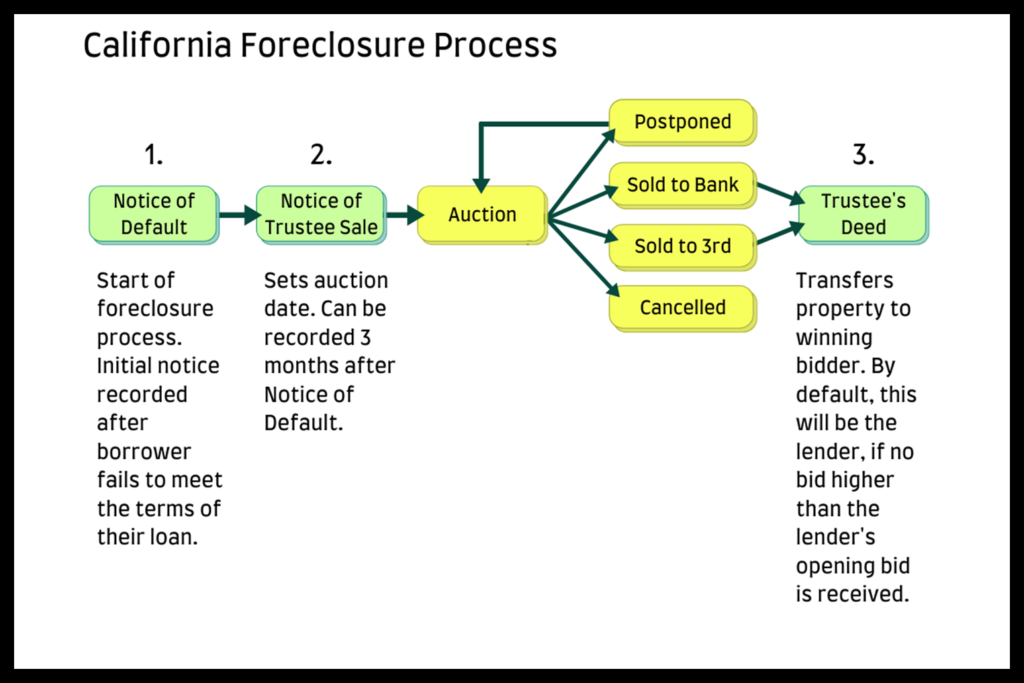

The California Notice of Default Timeline (Step-by-Step)

Foreclosure in California follows a predictable sequence. Visual timelines and diagrams are especially helpful for understanding how these stages connect and where urgency increases.

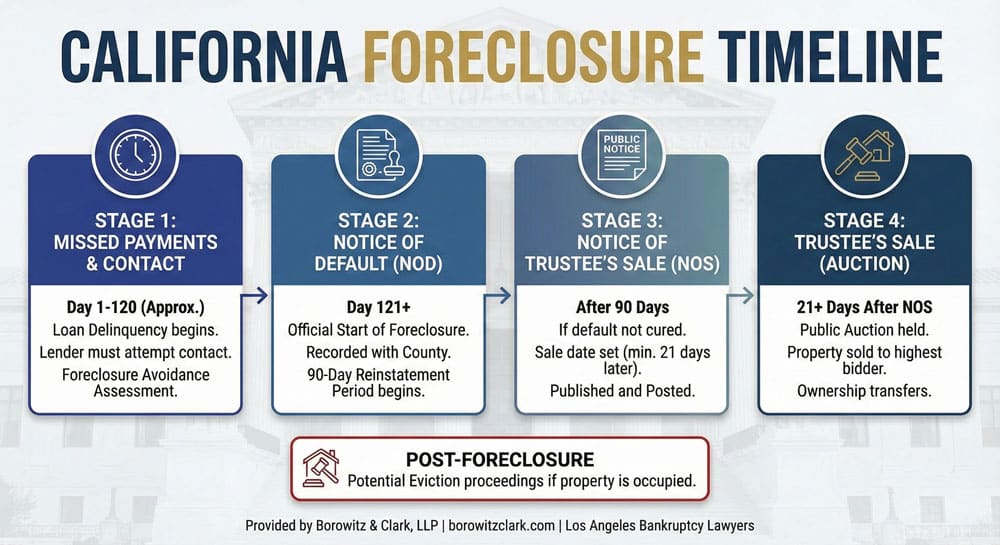

Stage 1: Missed Mortgage Payments (0–90 Days)

Before a Notice of Default is recorded, most homeowners have already missed several payments.

During this stage:

- Late fees and penalties may accrue

- Lenders may send notices or attempt contact

- Some loss mitigation options may still be available

This early phase is often overlooked, but it is when homeowners typically have the most flexibility.

Stage 2: Notice of Default Is Recorded (Around Day 90)

After approximately 90 days of delinquency, the lender may record a Notice of Default with the county recorder.

At this point:

- The foreclosure process officially begins

- Credit damage may already be occurring

- The foreclosure timeline is now governed by California law

No foreclosure sale can happen immediately after the Notice of Default is recorded.

Stage 3: 90-Day Reinstatement Period

California law requires a minimum 90-day waiting period after the Notice of Default is recorded before a foreclosure sale can be scheduled.

This period is critical.

During these 90 days, homeowners may:

- Reinstate the loan by catching up missed payments

- Apply for loan modification or forbearance

- Sell the property

- Explore other exit strategies

A visual timeline showing this reinstatement window often helps homeowners understand how much time they realistically have to act.

Stage 4: Notice of Trustee Sale (After the 90 Days)

If the default is not resolved, the lender may record a Notice of Trustee Sale.

This notice:

- Sets a foreclosure auction date

- Must be issued at least 21 days before the sale

- Is mailed, posted on the property, and publicly advertised

Once this notice is recorded, the process accelerates significantly.

Stage 5: Foreclosure Auction (Approximately 120–180 Days Total)

If no action is taken, the property may be sold at public auction.

Key facts:

- Most California foreclosures are non-judicial

- There is typically no court hearing

- Ownership can transfer quickly after the auction

After this point, homeowner options are extremely limited.

How Long Does Foreclosure Take in California?

While timelines vary, a typical California foreclosure process looks like this:

- ~90 days delinquent before Notice of Default

- 90 days after the Notice of Default

- 21+ days after the Notice of Trustee Sale

Total estimated timeline: approximately 4 to 6 months, though delays can occur depending on lender actions or homeowner intervention.

Common Mistakes Homeowners Make After a Notice of Default

Many homeowners unintentionally reduce their options by:

- Ignoring official notices

- Waiting too long to act

- Assuming foreclosure is immediate

- Relying on unverified online advice

- Making rushed decisions under pressure

The most damaging mistake is doing nothing.

Can You Sell a House After Receiving a Notice of Default?

Yes. In many cases, homeowners can still sell their home after receiving a Notice of Default, and sometimes even after a Notice of Trustee Sale.

Selling before foreclosure may:

- Protect credit

- Preserve remaining equity

- Avoid eviction

- Provide a clean and controlled exit

A visual comparison between selling before foreclosure versus after auction often helps homeowners understand why timing matters.

Why Early Action Matters

The earlier a homeowner understands the Notice of Default timeline, the more control they usually have.

Early action often means:

- More available options

- Less financial damage

- Reduced stress

- Better long-term outcomes

Waiting until the foreclosure sale date dramatically limits flexibility.

Important Disclaimer

This article is provided for educational purposes only and does not constitute legal or financial advice. Foreclosure laws and timelines can change, and individual circumstances vary.

Homeowners facing a Notice of Default should consider consulting:

- A qualified real estate attorney

- A HUD-approved housing counselor

- A licensed financial or real estate professional

About the Author & Editorial Standards

This article was written and reviewed by real estate professionals with hands-on experience helping California homeowners navigate distressed property situations, including Notice of Default, pre-foreclosure, probate, and inherited property sales.

Editorial standards emphasize:

- Accuracy over urgency

- Education over fear-based messaging

- Clear explanations supported by real-world experience

Content is reviewed regularly to ensure accuracy and relevance.

Final Thoughts on the California Notice of Default Timeline

A Notice of Default is serious, but it does not automatically mean foreclosure is inevitable.

Understanding the California Notice of Default timeline empowers homeowners to make informed decisions, recognize their options, and take action before deadlines remove flexibility.

If you have questions about your situation or need clarity on next steps, feel free to reach out.